|

|

|

This documentation is now deprecated. Please switch to the IBKR Campus for up-to-date information regarding IBKR's API solutions. |

|

|

|

This documentation is now deprecated. Please switch to the IBKR Campus for up-to-date information regarding IBKR's API solutions. |

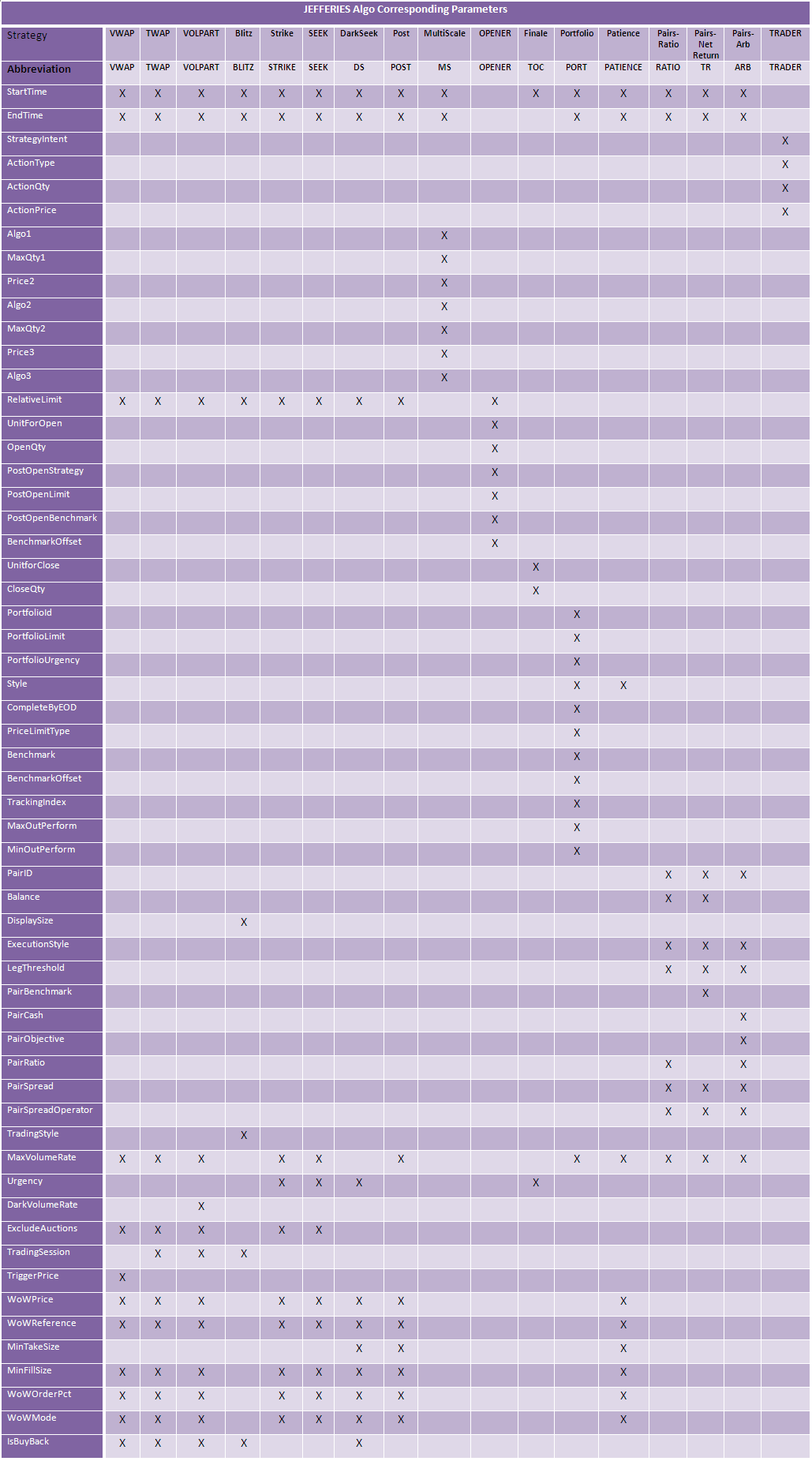

The Jefferies Algos are available with the socket-based API languages (Java, C#/.NET, Python, C++).

The following table lists all available Jefferies algo strategies and parameters supported by the API.

| Parameter | Description | Type | Syntax/Values |

|---|---|---|---|

| StartTime | Start time | Time | 9:00:00 EST |

| EndTime | End time | Time | 15:00:00 EST |

| Relative Limit | Double | Positive and negative values allowed. | |

| MaxVolumeRate | Double | ||

| ExcludeAuctions | Define auction participation | String | "Exclude_Both", "Include_Open", "Include_Close", "Include_Both" |

| TriggerPrice | Double | Any positive value, no max. | |

| WoWPrice | Would or Work - The price at which the user is willing to complete the order. Used if no WoW reference is specified. | Double | |

| WowReference | Used with WoW price field. If WoW price is not submitted, the Reference price can be submitted for processing. | String | "Market", "Inside_NBBO_Price", "Arrival Price", "PNC", "Open", "BPS_Arrival", "Price", "OPP", "Midpoint" |

| MinFillSize | Minimum number of share per execution for non-displayed liquidity. Rounded down to closest lot size. | Integer | |

| WoWOrderPct | Max percent of the order on which WoW can work. | Integer | |

| WoWMode | String | "BLITZ", "DARKSeek", "Seek_Passive", "Seek_Active", "Seek_Aggressive", "Volume_10%", "Volume_20%", "Volume_30%","VWAP_Day", "Patience" | |

| IsBuyBack | The algo should engage in SEC Rule 10b-18 restrictions for buy back in US securities. | String | "Yes", "No" |

Example Jefferies VWAP Algo

| Parameter | Description | Type | Syntax/Values |

|---|---|---|---|

| StartTime | Start time | Time | 9:00:00 EST |

| EndTime | End time | Time | 15:00:00 EST |

| Relative Limit | Double | Positive and negative values allowed. | |

| MaxVolumeRate | Double | ||

| ExcludeAuctions | Define auction participation | String | "Exclude_Both", "Include_Open", "Include_Close", "Include_Both" |

| TradingSession | Denotes the trading session for the order. | String | "DAY", "PRE-OPEN", "AFTER-HOURS" |

| WoWPrice | Would or Work - The price at which the user is willing to complete the order. Used if no WoW reference is specified. | Double | |

| WowReference | Used with WoW price field. If WoW price is not submitted, the Reference price can be submitted for processing. | String | "Market", "Inside_NBBO_Price", "Arrival Price", "PNC", "Open", "BPS_Arrival", "Price", "OPP", "Midpoint" |

| MinFillSize | Minimum number of share per execution. Rounded down to closest lot size. | Integer | |

| WoWOrderPct | Max percent of the order on which WoW can work. | Integer | |

| WoWMode | String | "BLITZ", "DARKSeek", "Seek_Passive", "Seek_Active", "Seek_Aggressive", "Volume_10%", "Volume_20%", "Volume_30%","VWAP_Day", "Patience" | |

| IsBuyBack | The algo should engage in SEC Rule 10b-18 restrictions for buy back in US securities. | String | "Yes", "No" |

| Parameter | Description | Type | Syntax/Values |

|---|---|---|---|

| StartTime | Start time | Time | 9:00:00 EST |

| EndTime | End time | Time | 15:00:00 EST |

| Relative Limit | Double | Positive and negative values allowed. | |

| MaxVolumeRate | Volume limit | Double | |

| DarkVolumeRate | Dark volume limit | Double | |

| ExcludeAuctions | Define auction participation | String | "Exclude_Both", "Include_Open", "Include_Close", "Include_Both" |

| TradingSession | Denotes the trading session for the order. | String | "DAY", "PRE-OPEN", "AFTER-HOURS" |

| WoWPrice | Would or Work - The price at which the user is willing to complete the order. Used if no WoW reference is specified. | Double | |

| WowReference | Used with WoW price field. If WoW price is not submitted, the Reference price can be submitted for processing. | String | "Market", "Inside_NBBO_Price", "Arrival Price", "PNC", "Open", "BPS_Arrival", "Price", "OPP", "Midpoint" |

| MinFillSize | Minimum number of share per execution for non-displayed liquidity. Rounded down to closest lot size. | Integer | |

| WoWOrderPct | Max percent of the order on which WoW can work. | Integer | |

| WoWMode | String | "BLITZ", "DARKSeek", "Seek_Passive", "Seek_Active", "Seek_Aggressive", "Volume_10%", "Volume_20%", "Volume_30%","VWAP_Day", "Patience" | |

| IsBuyBack | The algo should engage in SEC Rule 10b-18 restrictions for buy back in US securities. | String | "Yes", "No" |

| Parameter | Description | Type | Syntax/Values |

|---|---|---|---|

| StartTime | Start time | Time | 9:00:00 EST |

| EndTime | End time | Time | 15:00:00 EST |

| Relative Limit | Double | Positive and negative values allowed. | |

| DisplaySize | Integer | ||

| TradingStyle | String | "Price Improvement", "Opportunistic", "Get-It-Done", "No_Post" | |

| IsBuyBack | The algo should engage in SEC Rule 10b-18 restrictions for buy back in US securities. | String | "Yes", "No" |

| TradingSession | Denotes the trading session for the order. | String | "DAY", "PRE-OPEN", "AFTER-HOURS" |

| Parameter | Description | Type | Syntax/Values |

|---|---|---|---|

| StartTime | Start time | Time | 9:00:00 EST |

| EndTime | End time | Time | 15:00:00 EST |

| Relative Limit | Double | Positive and negative values allowed. | |

| MaxVolumeRate | Double | ||

| Urgency | String | "Passive", "Active", "Aggressive" | |

| ExcludeAuctions | Define auction participation | String | "Exclude_Both", "Include_Open", "Include_Close", "Include_Both" |

| WoWPrice | Would or Work - The price at which the user is willing to complete the order. Used if no WoW reference is specified. | Double | |

| WowReference | Used with WoW price field. If WoW price is not submitted, the Reference price can be submitted for processing. | String | "Market", "Inside_NBBO_Price", "Arrival Price", "PNC", "Open", "BPS_Arrival", "Price", "OPP", "Midpoint" |

| MinFillSize | Minimum number of share per execution for non-displayed liquidity. Rounded down to closest lot size. | Integer | |

| WoWOrderPct | Max percent of the order on which WoW can work. | Integer | |

| WoWMode | String | "BLITZ", "DARKSeek", "Seek_Passive", "Seek_Active", "Seek_Aggressive", "Volume_10%", "Volume_20%", "Volume_30%","VWAP_Day", "Patience" |

| Parameter | Description | Type | Syntax/Values |

|---|---|---|---|

| StartTime | Start time | Time | 9:00:00 EST |

| EndTime | End time | Time | 15:00:00 EST |

| Relative Limit | Double | Positive and negative values allowed. | |

| ExcludeAuctions | Define auction participation | String | "Exclude_Both", "Include_Open", "Include_Close", "Include_Both" |

| Urgency | String | "Passive_Minus", "Passive", "Active", "Active_Plus", "Aggressive" | |

| MaxVolumeRate | Double | ||

| WoWPrice | Would or Work - The price at which the user is willing to complete the order. Used if no WoW reference is specified. | Double | |

| WowReference | Used with WoW price field. If WoW price is not submitted, the Reference price can be submitted for processing. | String | "Market", "Inside_NBBO_Price", "Arrival Price", "PNC", "Open", "BPS_Arrival", "Price", "OPP", "Midpoint" |

| MinFillSize | Minimum number of share per execution for non-displayed liquidity. Rounded down to closest lot size. | Integer | |

| WoWOrderPct | Max percent of the order on which WoW can work. | Integer | |

| WoWMode | String | "BLITZ", "DARKSeek", "Seek_Passive", "Seek_Active", "Seek_Aggressive", "Volume_10%", "Volume_20%", "Volume_30%","VWAP_Day", "Patience" |

| Parameter | Description | Type | Syntax/Values |

|---|---|---|---|

| StartTime | Start time | Time | 9:00:00 EST |

| EndTime | End time | Time | 15:00:00 EST |

| Relative Limit | Double | Positive and negative values allowed. | |

| Urgency | String | "Passive_Minus", "Passive", "Active", "Active_Plus", "Aggressive" | |

| MinTakeSize | Minimum number of share per execution for displayed liquidity. Rounded down to closest lot size. | Integer | |

| MinFillSize | Minimum number of share per execution for non-displayed liquidity. Rounded down to closest lot size. | Integer | |

| IsBuyBack | The algo should engage in SEC Rule 10b-18 restrictions for buy back in US securities. | String | "Yes", "No" |

| WoWPrice | Would or Work - The price at which the user is willing to complete the order. Used if no WoW reference is specified. | Double | |

| WowReference | Used with WoW price field. If WoW price is not submitted, the Reference price can be submitted for processing. | String | "Market", "Inside_NBBO_Price", "Arrival Price", "PNC", "Open", "BPS_Arrival", "Price", "OPP", "Midpoint" |

| WoWOrderPct | Max percent of the order on which WoW can work. | Integer | |

| WoWMode | String | "BLITZ", "DARKSeek", "Seek_Passive", "Seek_Active", "Seek_Aggressive", "Volume_10%", "Volume_20%", "Volume_30%","VWAP_Day", "Patience" |

| Parameter | Description | Type | Syntax/Values |

|---|---|---|---|

| StartTime | Start time | Time | 9:00:00 EST |

| EndTime | End time | Time | 15:00:00 EST |

| Relative Limit | Double | Positive and negative values allowed. | |

| MaxVolumeRate | Volume limit. | Double | |

| WoWPrice | Would or Work - The price at which the user is willing to complete the order. Used if no WoW reference is specified. | Double | |

| WowReference | Used with WoW price field. If WoW price is not submitted, the Reference price can be submitted for processing. | String | "Market", "Inside_NBBO_Price", "Arrival Price", "PNC", "Open", "BPS_Arrival", "Price", "OPP", "Midpoint" |

| MinTakeSize | Minimum number of share per execution for displayed liquidity. Rounded down to closest lot size. | Integer | |

| MinFillSize | Minimum number of share per execution for non-displayed liquidity. Rounded down to closest lot size. | Integer | |

| WoWOrderPct | Max percent of the order on which WoW can work. | Integer | |

| WoWMode | String | "BLITZ", "DARKSeek", "Seek_Passive", "Seek_Active", "Seek_Aggressive", "Volume_10%", "Volume_20%", "Volume_30%","VWAP_Day", "Patience" |

| Parameter | Description | Type | Syntax/Values |

|---|---|---|---|

| StartTime | Start time | Time | 9:00:00 EST |

| EndTime | End time | Time | 15:00:00 EST |

| Algo1 | The base algo. | String | "Volume_5%", "Volume_10%", "Volume_15%", "Volume_20%", "Volume_25%", "Volume_30%", "DARKSeek", "Seek_Passive", "Seek_Active", "Seek_Aggressive", "BLITZ", "VWAP_Day", "Qty_Scale", "Patience" |

| MaxQty1 | Max quantity for the base algo. | Integer | |

| Price 2 | Trigger price for algo 2 if present. | Double | |

| Algo2 | Underlying algo 2. Must be different than Algo1 or Algo3. | String | "Volume_5%", "Volume_10%", "Volume_15%", "Volume_20%", "Volume_25%", "Volume_30%", "DARKSeek", "Seek_Passive", "Seek_Active", "Seek_Aggressive", "BLITZ", "VWAP_Day", "Qty_Scale", "Patience" |

| MaxQty2 | Max quantity for algo 2 | Integer | |

| Price3 | Trigger price for algo 3 if present. | String | |

| Algo3 | Underlying algo 2. Must be different than Algo1 or Algo2. | String | "Volume_5%", "Volume_10%", "Volume_15%", "Volume_20%", "Volume_25%", "Volume_30%", "DARKSeek", "Seek_Passive", "Seek_Active", "Seek_Aggressive", "BLITZ", "VWAP_Day", "Qty_Scale", "Patience" |

| Parameter | Description | Type | Syntax/Values |

|---|---|---|---|

| Relative Limit | Double | Positive and negative values allowed. | |

| UnitForOpen | Defines the unit for the open quantity, either shares or percentage. | String | Shares must be in round lots. Percentage must be between 1 and 100. |

| OpenQty | Determines quantity placed into opening auction. Used unit defined in UnitForOpen. | Double | |

| PostOpenStrategy | String | "Volume_5%", "Volume_10%", "Volume_15%", "Volume_20%", "Volume_25%", "Volume_30%", "DARKSeek", "Seek_Passive", "Seek_Active", "Seek_Aggressive", "BLITZ", "VWAP_Day", "Qty_Scale", "Patience" | |

| PostOpenLimit | Absolute limit price for the Post Open strategy. | Double | |

| PostOpenBenchmark | String | "Inside_NBBO_Price", "Arrival_Price", "PNC", "Open" | |

| BenchmarkOffset | In conjunction with Post Open Benchmark, this sets the relative limit for the strategy. | Integer | Positive or negative value in basis points set as the relative limit from the post open benchmark. |

| Parameter | Description | Type | Syntax/Values |

|---|---|---|---|

| StartTime | Start time | Time | 9:00:00 EST |

| Urgency | String | "Passive", "Active", "Aggressive" | |

| UnitForClose | The unit to use when defining the close quantity. | String | "Shares", "%_of_Order", "%_of_ADV", "%_of_Expected_Close" |

| CloseQty | The quantity of the closing auction. | Double |

| Parameter | Description | Type | Syntax/Values |

|---|---|---|---|

| StartTime | Start time | Time | 9:00:00 EST |

| EndTime | End time | Time | 15:00:00 EST |

| MaxVolumeRate | Double | ||

| PortfolioId | User defined ID | FixSizeString | |

| PortfolioLimit | Basis points from arrival | Double | |

| ExcludeAuctions | Define auction participation | String | "Exclude_Both", "Include_Open", "Include_Close", "Include_Both" |

| PortfolioUrgency | String | "1", "2", "3", "4", "5" | |

| Style | String | "Cash_Balance", "Beta_Neutral", "IS", "Dark_Only", "Exec_Balance" | |

| CompleteByEOD | String | "Yes", "No" | |

| PriceLimitType | String | "Fixed", "Floating" | |

| Benchmark | String | "Inside_NBBO_Price", "Arrival_Price", "PNC", "Open" | |

| BenchmarkOffset | Integer | Positive or Negative value in basis points. | |

| TrackingIndex | FixSizeString | ||

| MaxOutPerform | Integer | Positive or Negative value in basis points. | |

| MinOutPerform | Integer | Positive or Negative value in basis points. |

| Parameter | Description | Type | Syntax/Values |

|---|---|---|---|

| StartTime | Start time | Time | 9:00:00 EST |

| EndTime | End time | Time | 15:00:00 EST |

| MaxVolumeRate | Volume limit. | Double | |

| Style | Boolean | ||

| WoWPrice | Would or Work - The price at which the user is willing to complete the order. Used if no WoW reference is specified. | Double | |

| WowReference | Used with WoW price field. If WoW price is not submitted, the Reference price can be submitted for processing. | String | "Market", "Inside_NBBO_Price", "Arrival Price", "PNC", "Open", "BPS_Arrival", "Price", "OPP", "Midpoint" |

| MinTakeSize | Minimum number of share per execution for displayed liquidity. Rounded down to closest lot size. | Integer | |

| MinFillSize | Minimum number of share per execution for non-displayed liquidity. Rounded down to closest lot size. | Integer | |

| WoWOrderPct | Max percent of the order on which WoW can work. | Integer | |

| WoWMode | String | "BLITZ", "DARKSeek", "Seek_Passive", "Seek_Active", "Seek_Aggressive", "Volume_10%", "Volume_20%", "Volume_30%","VWAP_Day", "Patience" |

| Parameter | Description | Type | Syntax/Values |

|---|---|---|---|

| StartTime | Start time | Time | 9:00:00 EST |

| EndTime | End time | Time | 15:00:00 EST |

| MaxVolumeRate | Volume limit. | Double | |

| PairID | FixSizeString | ||

| Balance | String | "Share_Balanced", "Cash_Balanced", "Ratio_Balanced" | |

| ExecutionStyle | String | "Active", "TWAP", "Aggressive", "Custom" | |

| LegThreshold | Double | ||

| PairRatio | Double | ||

| PairSpread | Double | ||

| PairSpreadOperator | String | <=, >= |

| Parameter | Description | Type | Syntax/Values |

|---|---|---|---|

| StartTime | Start time | Time | 9:00:00 EST |

| EndTime | End time | Time | 15:00:00 EST |

| MaxVolumeRate | Volume limit. | Double | |

| PairID | FixSizeString | ||

| Balance | String | "Share_Balanced", "Cash_Balanced", "Ratio_Balanced" | |

| ExecutionStyle | String | "Active", "TWAP", "Aggressive", "Custom" | |

| LegThreshold | Double | ||

| PairBenchmark | String | "PNC", "Open", "Arrival_Price" | |

| PairSpread | Double | ||

| PairSpreadOperator | String | <=, >= |

| Parameter | Description | Type | Syntax/Values |

|---|---|---|---|

| StartTime | Start time | Time | 9:00:00 EST |

| EndTime | End time | Time | 15:00:00 EST |

| MaxVolumeRate | Volume limit. | Double | |

| ExecutionStyle | String | "Active", "TWAP", "Aggressive", "Custom" | |

| LegThreshold | Double | ||

| PairID | FixSizeString | ||

| PairObjective | String | "Setup", "Unwind", "Reverse" | |

| PairRatio | Double | ||

| PairCash | Double | ||

| PairSpread | Double | ||

| PairSpreadOperator | String | <=, >= |

| Parameter | Description | Type | Syntax/Values |

|---|---|---|---|

| StrategyIntent | String | "Volume_5%", "Volume_10%", "Volume_15%", "Volume_20%", "Volume_25%", "Volume_30%", "DARKSeek", "Seek_Passive", "Seek_Active", "Seek_Aggressive", "BLITZ", "VWAP_Day", "Qty_Scale", "Patience" | |

| ActionType | String | "Halt", "Resume", "Check_Dark", "Take/Hit" | |

| ActionQty | Integer | ||

| ActionPrice | Double |